Can a portfolio look diversified on paper but still behave like one concentrated bet when markets come under pressure?

Family offices have increased allocations to alternatives in search of diversification, resilience, and stronger risk-adjusted returns. But beneath the surface, many private markets portfolios may share the same managers, companies, sectors, leverage structures, and macro drivers. That hidden overlap is creating a new risk: shadow correlation.

For many family offices, the alternatives portfolio looks well spread out.

There may be private equity, private credit, venture capital, real estate, hedge funds, infrastructure, secondaries, and multiple managers. On paper, that can look like diversification.

But the labels may be doing more work than the actual exposures.

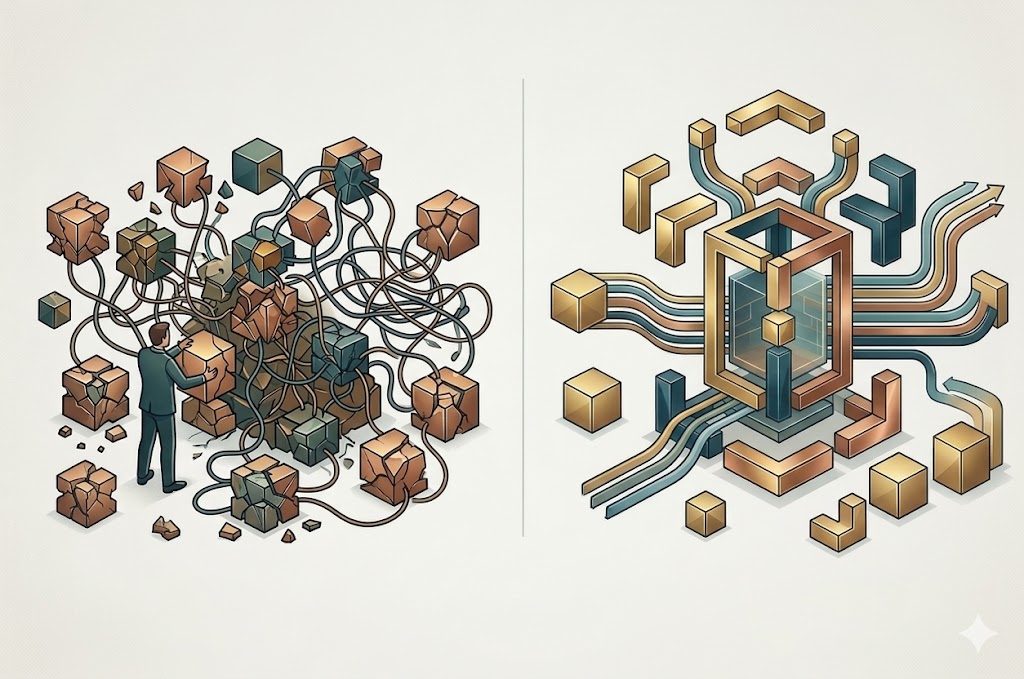

A family office may believe it is diversified across five managers, only to discover that those managers are lending to, investing in, or acquiring the same companies. The same sectors may dominate deal flow. The same general partners may raise capital across multiple strategies. The same macro pressures may affect private equity, private credit, real estate, infrastructure, and secondaries at the same time.

That is the problem of shadow correlation.

When Diversification Becomes Less Diversifying

Family offices have spent the past decade increasing allocations to alternatives. The goal has often been clear: improve risk-adjusted returns, reduce reliance on public markets, add inflation resilience, and access return streams with lower apparent correlation.

The challenge is that apparent diversification can be misleading.

Shadow correlation occurs when strategies appear diversified but share overlapping underlying drivers. These can include:

- Company and sector exposure

- Manager and GP overlap

- Valuation assumptions

- Leverage structures

- Credit conditions

- Exit market dependency

- Interest rate sensitivity

Because investments are often classified by asset class, strategy, or manager, portfolios can look more diversified than they really are.

A private equity fund, a private credit fund, a secondaries fund, and a real estate strategy may sit in different portfolio buckets. But if they are exposed to similar financing conditions, sponsor ecosystems, valuation cycles, and liquidity constraints, they may behave more similarly than expected during stress.

Private Markets Are More Connected Than They Look

The private markets ecosystem has become more concentrated and more interconnected.

Large alternative asset managers now operate across buyout, private credit, real estate, infrastructure, and secondaries. According to the source article, the five largest private market managers — Apollo, Ares, Blackstone, Carlyle, and KKR — now manage a combined $1.5 trillion in perpetual capital.

This matters because the same manager ecosystems can appear across multiple parts of a family office portfolio.

Private equity and private credit are especially linked. Many buyout-backed companies rely on private credit financing. Some secondaries funds buy stakes in funds that family offices may already hold. NAV financing, sponsor-backed lending, and fund-level leverage can create additional connections beneath the surface.

The result is a network of exposure that is often much more connected than traditional portfolio reporting suggests.

Macro Pressure Can Reveal the Linkages

Shadow correlation becomes most visible when conditions tighten.

Rising interest rates, slower exit markets, tighter credit conditions, and geopolitical risk can affect several private markets strategies at once. Private equity valuations may come under pressure. Private credit underwriting may become more sensitive. Real estate and infrastructure may feel the impact of higher financing costs. Distributions may slow across the board.

That creates a different kind of risk.

The portfolio may not be concentrated in one fund or one asset class, but it may still be concentrated in the same economic assumptions.

The source article highlights several pressure points:

- In 2025, 13 mega-deals valued at $10 billion or more accounted for 69% of total growth in buyout deal value.

- Around 30% of US private equity inventory was held for seven years or longer.

- Private credit has become increasingly intertwined with private equity through sponsor-backed lending, NAV financing, and fund-level leverage.

For family offices, this means correlation analysis cannot stop at the asset class label.

The Questions Family Offices Need to Ask

The first step is not necessarily changing the portfolio. It is understanding what the portfolio actually owns.

Three questions are especially important:

Do we have a full look-through view of our private markets exposures?

If not, the family office may need a consolidated exposure map across managers, sectors, companies, funds, and strategies.

Are our private equity, private credit, and secondaries exposures linked beneath the surface?

If yes, pacing, liquidity buffers, and risk models may need to reflect those linkages.

Do we have a liquidity framework that accounts for correlated capital calls and delayed distributions?

If not, the office may need to build a liquidity waterfall and test scenarios where capital calls rise while distributions slow.

These questions are operational as much as investment-related. Without the right reporting, data aggregation, and look-through visibility, shadow correlation can remain hidden until stress makes it obvious.

What Stronger Investment Processes Look Like

Family offices do not need to treat shadow correlation as a reason to step away from alternatives. The more practical response is to make the investment process more correlation-aware.

That means building better visibility across the whole portfolio.

Key steps include:

- Building a look-through exposure map across private markets

- Testing for GP overlap, sector clustering, and cross-strategy linkages

- Developing risk models that include private equity, private credit, secondaries, real estate, and infrastructure together

- Creating pacing and liquidity governance that reflects delayed distributions and correlated capital calls

- Understanding the relationship between public and private market holdings

- Considering whether additional diversifiers, such as infrastructure, energy, or real assets, change the portfolio’s true exposure profile

- Investing in reporting technology that improves real-time visibility

The goal is not perfect prediction. It is better awareness of where diversification may be weaker than it appears.

Visibility Is Becoming a Strategic Advantage

Shadow correlation is not a temporary feature of private markets. It is a structural consequence of consolidation, leverage, and the increasing interconnectedness of global capital.

For family offices, that makes visibility more important than ever.

A portfolio that looks diversified by manager or asset class may still carry concentrated exposure to the same companies, sectors, financing conditions, and liquidity cycles. The offices that understand those linkages earlier will be better positioned to manage pacing, liquidity, and risk through market stress.

In a more connected private markets environment, the advantage may not come from having more data. It may come from seeing the hidden relationships inside the data clearly enough to act with discipline.

To see how Altius can help family offices improve portfolio visibility, streamline reporting, and identify hidden exposures across complex investments, contact the Altius team to book a demo.